Understanding Taxation on 2nd and 3rd Pillar Withdrawals in Switzerland

How Your Canton and Withdrawal Amount Affect Your Tax Rate

Posted by

Related reading

5% Over CHF 5 Million: National Inheritance Tax Reloaded

5% Over CHF 5 Million: National Inheritance Tax Reloaded

The 10 Million Limit: UBS Analyzes the Real Estate Impact

The 10 Million Limit: UBS Analyzes the Real Estate Impact

Swiss Housing Scarcity: The 10-Year Record Low in Homes on the Market

Swiss Housing Scarcity: The 10-Year Record Low in Homes on the Market

When retiring or withdrawing from your pension systems (i.e. 2nd and/or 3rd pillar) be it for retirement or buying property or for starting a company - your domicile plays a significant role.

This means when withdrawing from your 2nd and 3rd pillar pension funds in Switzerland, the taxes you'll pay can vary significantly based on the canton or municipality you live in. While these withdrawals are taxed at a lower rate than regular income, several factors influence how much you'll ultimately pay.

1. Taxation of 2nd and 3rd Pillar Withdrawals

Pension withdrawals are taxed separately from your regular income, often at a reduced rate. However, the tax is progressive, meaning the more you withdraw, the higher the tax percentage. Additionally, each canton and municipality applies different rates, so your location when withdrawing plays a crucial role.

2. Approximate Tax Rates

Here's a general idea of how much you might pay:

Smaller Withdrawals (CHF 50,000): Tax rates typically range from 2% to 10%, depending on the canton.

Larger Withdrawals (CHF 500,000): For bigger amounts, rates can rise to 10% to 20%.

Examples by Canton:

- Zug: Known for low taxes, withdrawals of CHF 200,000 may be taxed at around 5-7%.

- Zurich: In Zurich, tax rates for similar amounts might be slightly higher, ranging between 7-10%.

- Schwyz: Similar to Zug, Schwyz offers attractive rates, with 5-6% for mid-sized withdrawals.

3. Using Tax Simulation Tools

Many cantons provide online tax calculators where you can estimate your tax burden based on your withdrawal amount. These tools are a great resource for planning your finances and understanding your tax obligations.

Important: This article shall not substitute any tax advice and we recommend consulting a tax advisor before making any decisions on your withdrawals from your second or third pillar.

If you are planning a withdrawal or looking to relocate to a low-tax area for retirement, consider using LowTaxHomes.ch to find your next home in a tax-friendly municipality.

---

The Massive Cantonal Disparity

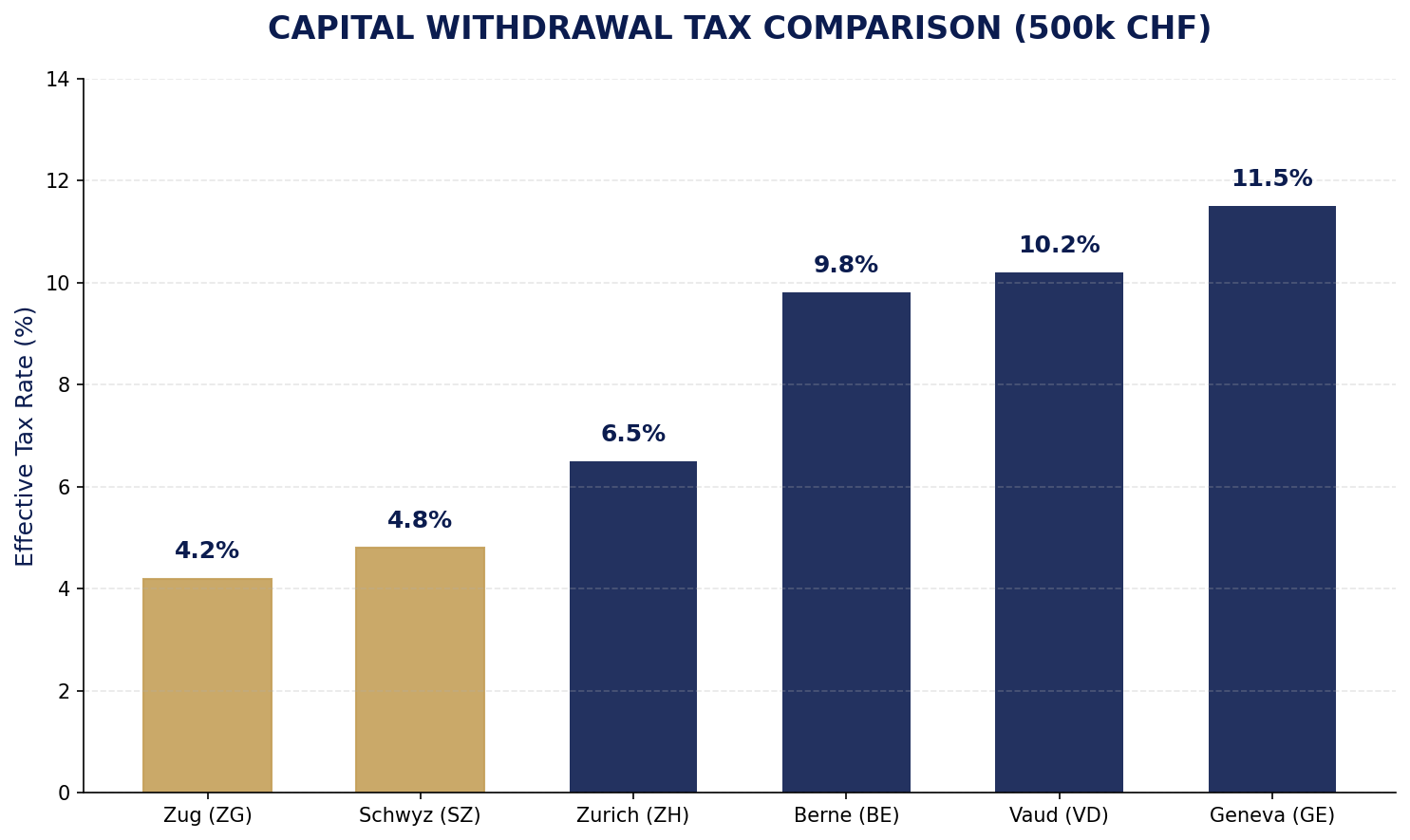

Withdrawing your retirement capital in Switzerland is not taxed at a flat rate. The tax burden varies dramatically depending on your legal residence at the moment of withdrawal. While high-tax cantons like Geneva or Vaud can claim over 11% of your savings, the low-tax havens of Zug and Schwyz remain the golden standard for wealth preservation.

Fig 1: Estimated capital withdrawal tax rates (Federal + Cantonal + Communal) for a 500,000 CHF withdrawal. Data based on 2024/2025 LTH analysis.

Verified Tax Simulation Tools

For a precise, personalized calculation, we recommend utilizing these official and industry-standard simulators:

1. Finpension Capital Withdrawal Tax Calculator – Excellent for comparing all 26 cantons side-by-side.

2. Vermoegenszentrum (VZ) Tax Calculator – Comprehensive for Pillar 2, Pillar 3, and AHV calculations.

3. ESTV (Federal Tax Administration) Simulator – The official government tool for binding federal and cantonal estimates.

The Low-Tax Strategy

The difference between withdrawing 500,000 CHF in Geneva (11.5% tax) versus Zug (4.2% tax) amounts to a staggering 36,500 CHF in pure savings. This is why strategic relocation within Switzerland before your retirement pivot is one of the most effective wealth management moves available.

---

The Million-Franc Difference: Geneva vs. Zug

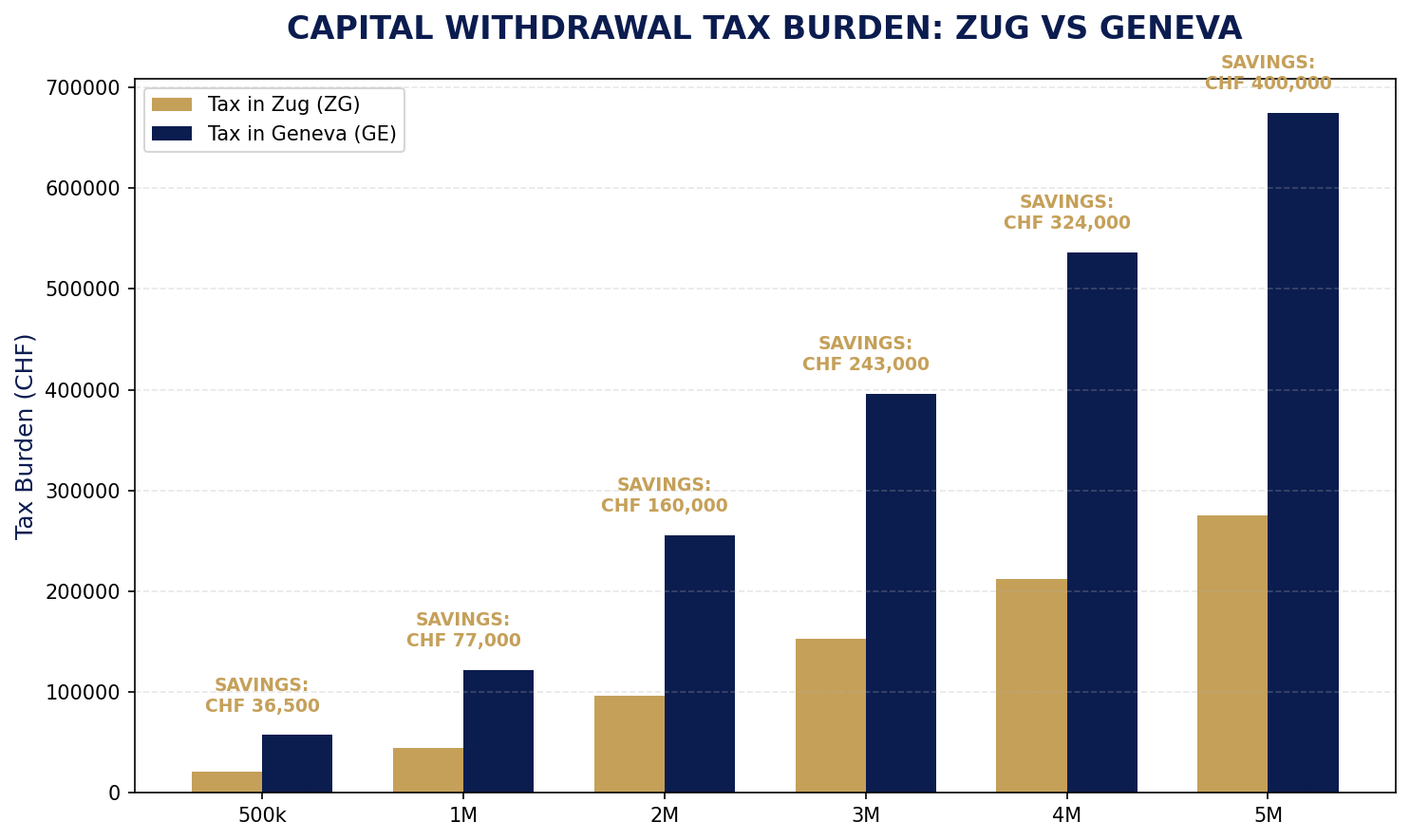

The "Low-Tax Strategy" is most powerful when applied to significant pension assets. While a 500,000 CHF withdrawal already yields a 36,500 CHF saving in Zug compared to Geneva, the gap widens exponentially as assets grow. In high-tax cantons like Geneva, Vaud, or Berne, the progressive nature of capital withdrawal tax can erode a massive portion of your life's work.

Fig 2: Comparative tax burden for high-value capital withdrawals. Calculations based on 2024/2025 cantonal tax scales for single taxpayers.

#### The Strategic Breakdown:

- 500k CHF Withdrawal: Geneva (~57.5k) vs. Zug (~21k) = 36.5k CHF Saved

- 1M CHF Withdrawal: Geneva (~122k) vs. Zug (~45k) = 77k CHF Saved

- 2M CHF Withdrawal: Geneva (~256k) vs. Zug (~96k) = 160k CHF Saved

- 5M CHF Withdrawal: Geneva (~675k) vs. Zug (~275k) = 400k CHF Saved

For ultra-high-net-worth individuals, relocating to a low-tax municipality like Walchwil, Oberägeri, or Wollerau before the "retirement pivot" is not just a lifestyle choice—it is one of the most effective wealth management moves available in Switzerland.

Beyond the Withdrawal: The Triple-Benefit Strategy

Relocating to a low-tax canton like Zug or Schwyz offers more than just a one-time saving on your pillar withdrawal. It triggers a "Triple-Benefit" for your long-term wealth:

1. Wealth Tax Optimization: Cantons like Zug and Schwyz maintain some of the lowest wealth tax rates in Switzerland. For assets over 5M CHF, the difference between living in Geneva (up to 1%) versus Zug (~0.2%) can save you tens of thousands of francs every single year.

2. Superior Property Value Stability: Real estate in low-tax municipalities historically shows higher value retention and growth. Demand in Zug and the Schwyzer lakefront (Wollerau/Feusisberg) remains decoupled from broader market volatility due to the constant influx of high-tax-efficiency seeking buyers.

3. Income Tax Efficiency: If you continue to generate income post-retirement (via board seats, consulting, or investments), your annual tax bill will remain significantly lower, allowing for faster capital reinvestment.

At Lowtaxhomes, we specialize in connecting discerning buyers with properties that unlock these specific financial advantages. Positioning yourself in the right municipality today defines the legacy you leave tomorrow.

---

Secure Your Position in the Low-Tax Market

The demographic momentum of Switzerland is undeniable. Whether you are looking for a strategic primary residence or a high-yield investment, positioning yourself in the right municipality today defines your financial legacy.

Join Lowtaxhomes today to receive exclusive access to premium listings and expert tax insights before the market moves.

👉 Register for Property Alerts

👉 Explore Premium Listings

---